Skip to content

Skip to content

When you’re going through a divorce in Kingwood, the question of what happens to your retirement savings is often front and center. For many families in our community, these accounts are the most significant asset after the family home. In Texas, funds contributed to accounts like a 401(k) or pension during your marriage are typically considered community property and are subject to division. But it's not a simple 50/50 chop; Texas law requires a fair split based on your family's unique situation.

At The Law Office of Bryan Fagan, our goal is to provide our Kingwood neighbors with simple, practical legal advice. We want you to feel understood and supported as you navigate this process.

How Texas Law Views Your Retirement Accounts in a Kingwood Divorce

For many families we've worked with in Kingwood, Humble, and across Northeast Houston, these retirement accounts are the largest asset they own. Understanding how Texas law treats these funds is your first step toward protecting your financial future. The most important concept you'll need to grasp is community property.

Community vs. Separate Property

Here's a simple explanation: Texas law presumes that anything you or your spouse acquired from the day you got married until the day you divorce is community property. This absolutely includes the portion of your 401(k), IRA, or pension that grew from contributions and market gains during the marriage.

On the other hand, separate property is yours alone—it’s not up for division. This typically includes:

- Funds that were already in your retirement account before you were married.

- Gifts or inheritances that were given to only one spouse during the marriage, as long as they weren't mixed with community funds.

- The growth on those pre-marriage funds, but only if you can clearly trace it.

Proving what counts as separate property is all about the paper trail. This is why digging up old account statements is so important. If you can’t provide clear proof, a Kingwood court is likely to presume the entire account is community property.

To help clarify, here’s a quick breakdown of how these classifications typically work for retirement assets in a Kingwood divorce.

Community Property vs Separate Property in a Kingwood Divorce

| Asset Type | Classification | How It's Handled in a Kingwood Divorce |

|---|---|---|

| Contributions During Marriage | Community Property | The value of all contributions made by either spouse from the date of marriage to the date of divorce is subject to division. |

| Gains on Marital Contributions | Community Property | Any investment growth, interest, or dividends earned on the community portion of the account is also divisible. |

| Pre-Marriage Account Balance | Separate Property | The account balance as of the date of marriage is protected and belongs solely to the original owner. |

| Gains on Separate Property | Separate Property | Growth on the pre-marriage balance can remain separate if it can be clearly traced and has not been commingled with marital funds. |

| Inherited Retirement Accounts | Separate Property | An IRA or other account inherited by one spouse is generally their separate property, as long as it's kept apart from marital funds. |

This table provides a general overview, but tracing and proving the character of these funds often requires a detailed financial analysis from an experienced local attorney.

The "Just and Right" Division Standard

It's a common myth that community property always gets split down the middle. While a 50/50 division is frequent, Texas courts are legally required to make a "just and right" division. This gives the judge flexibility to divide the assets in a way they consider fair, which might look more like 60/40 or 55/45.

When dividing retirement assets, a Texas court will weigh multiple factors to achieve a fair outcome. This ensures the final division reflects the unique realities of your marriage and the needs of your family moving forward.

For instance, we’ve seen cases right here in Northeast Houston involving a long-term marriage where one spouse was a high-earning professional and the other was a stay-at-home parent. A judge might award the non-working spouse a larger percentage of the community retirement funds to recognize their non-financial contributions and account for their potentially lower earning power after the divorce.

Factors like the length of the marriage, each spouse's financial needs, who has custody of the children, and any fault in the breakup can all influence what the judge considers "just and right."

For a complete look at how all marital assets are handled, our guide on property division in a Kingwood divorce provides a much broader context for what to expect.

Understanding these core principles is the foundation for navigating the division of your retirement accounts. The Law Office of Bryan Fagan is here to offer the local, experienced guidance you need. We invite our neighbors in Kingwood, Humble, and Porter to schedule a free consultation to talk about your specific situation.

Getting a Handle on Your Retirement Assets: Identification and Valuation

Before you can begin talking about who gets what in a Kingwood divorce, you have to know exactly what you're working with. This starts with a full inventory of every single retirement account held by you and your spouse. Getting this right from the beginning is fundamental to protecting your financial future.

This means gathering the paperwork for every plan—401(k)s, 403(b)s, traditional and Roth IRAs, pensions, and more. You're essentially building a financial roadmap of your marriage, and these documents are your best tools for tracing what you brought into the marriage versus what you built together.

The Paper Chase: A Practical Step-by-Step Guide

Your most important task is to collect account statements that cover the entire span of your marriage. This timeline is not optional. Without it, telling the difference between your separate property and the community's share is incredibly difficult, and Texas law will assume everything is community property until you prove otherwise.

Here are the steps to get organized:

- Create a List: Make a simple list of all known retirement accounts for both you and your spouse.

- Gather Statements: Collect statements from around the date of your marriage and your most recent statements. This helps establish the separate property portion.

- Identify Plan Types: Note whether each account is an employer plan (like a 401(k) or pension) or an individual one (like an IRA). Military and federal pensions have their own complex rules.

If you believe your spouse isn't being completely upfront about their finances, gathering this information is even more critical. Our Kingwood attorneys frequently use formal discovery requests to compel the disclosure of all financial documents, ensuring nothing is missed. You can read more about that process in our guide on how to find hidden assets in divorce.

How Different Accounts Are Valued

Putting a number on these assets isn't always straightforward. The valuation method changes completely depending on the type of account. For instance, a 401(k) or an IRA is what we call a defined contribution plan. Its value is simply the cash balance in the account on a specific date, which you can find right on a statement.

Pensions, on the other hand, are defined benefit plans. They don't have a simple account balance; they promise a future monthly income stream. Their value has to be calculated using a formula based on the employee’s salary, years of service, and even their life expectancy.

Here’s a real-world scenario we see often with local couples in the Humble and Porter area. Let's say one spouse is a Humble ISD teacher with a TRS pension, and the other has a corporate 401(k).

- The 401(k) is easy to value. We just need statements from the date of marriage and a current one to determine the community property portion.

- The TRS pension is much more complicated. A financial expert may need to calculate its "present-day value" to determine what lump-sum amount is equivalent to those future payments.

For federal employees, knowing the ins and outs of a FERS pension is crucial. A helpful resource on this topic is this practical guide to the FERS Retirement Calculation.

When to Call in a Financial Expert

For many couples in the Kingwood area, especially those with long-term marriages or high-value estates, hiring a Certified Public Accountant (CPA) or a credentialed financial analyst is a very smart move. They can trace separate property claims, put a present-day value on a pension, or analyze complex assets like stock options. The cost of hiring an expert is almost always a fraction of what you could lose if the valuation is done incorrectly.

In marriages lasting more than a decade, retirement funds often represent a massive piece of the financial pie. Data from Texas family courts indicates these plans can make up, on average, 40% of the total community assets divided, with valuations frequently running into the hundreds of thousands of dollars.

Protecting your share of these hard-earned assets requires a sharp eye and meticulous work. If you're feeling overwhelmed, you are not alone. The team at The Law Office of Bryan Fagan is here to provide the support and guidance you need. Contact our Kingwood office for a free consultation to discuss your case and ensure your assets are identified and valued correctly.

The QDRO: Your Most Important Tool for Dividing Retirement Funds

After you've identified and valued all the retirement assets, the next step is actually dividing them. This is where a very specific, and absolutely critical, legal document comes into play: the Qualified Domestic Relations Order, or QDRO.

For our clients here in Kingwood and Porter, understanding the QDRO (pronounced "kwah-dro") is often the key to securing their financial future post-divorce.

A QDRO is a special court order that directs a retirement plan administrator to divide an account as part of a divorce settlement. For most private-sector retirement plans like 401(k)s, 403(b)s, and pensions, it's not optional. It is the only way to legally transfer those funds to an ex-spouse without triggering a massive tax bill.

Why You Cannot Afford to Skip This Step

Trying to divide a retirement account without a QDRO is one of the most expensive mistakes you can make in a divorce. The plan administrator has no choice but to treat the transfer as an early withdrawal, and the financial hit can be devastating.

Let’s look at a real-world scenario we often see in the Northeast Houston area:

A couple has a 401(k) with $200,000 in community property. The divorce decree awards the non-employee spouse half, or $100,000. Without a proper QDRO, here’s how that plays out:

- The IRS immediately requires a mandatory 20% federal income tax withholding on the $100,000 distribution. That's $20,000 gone right away.

- Because the account holder is under 59 ½, the IRS also levies a 10% early withdrawal penalty. Another $10,000 vanishes.

- To make matters worse, the full $100,000 is added to the employee spouse's taxable income for the year, likely pushing them into a higher tax bracket and resulting in thousands more owed.

That $100,000 award has suddenly shrunk to less than $70,000. A professionally drafted QDRO avoids this entire nightmare. It allows the funds to be rolled over directly and tax-free into the receiving spouse's own retirement account.

The Dangers of a Poorly Drafted QDRO

Unfortunately, just having a QDRO isn't enough—it has to be perfect. These are highly technical documents, and every retirement plan has its own strict, non-negotiable rules for what they will and will not accept.

One small mistake—a wrong account number, language the plan administrator rejects, or a missed deadline—will get the QDRO bounced.

A rejected QDRO means everything grinds to a halt. It creates delays, racks up more legal fees, and leaves your financial security in limbo while your attorney tries to fix it. The stakes are even higher than just inconvenience. For example, some legal analysis shows that if the employee spouse dies before a flawed QDRO is approved, the surviving ex-spouse could lose their entire share in about 15% of cases.

The QDRO is more than a legal formality; it's your financial shield. It protects the value of your awarded assets from crippling taxes and penalties, ensuring you receive the full share you are entitled to under your divorce decree.

Getting it right the first time is non-negotiable. You can read more about the complexities of dividing retirement assets and related risks at TheTexasAttorney.com.

This is precisely why you need an experienced Kingwood family law attorney to handle your QDRO from start to finish. Our team at The Law Office of Bryan Fagan has spent years mastering the intricate requirements of different plan administrators. We have a proven process to ensure every detail is correct, preventing rejections and securing your assets efficiently.

If you are facing a divorce in Kingwood, Humble, or the surrounding communities, don't leave the division of your retirement accounts to chance. Schedule a free, no-obligation consultation with our Kingwood office today to learn how we can protect your financial interests.

Negotiation Strategies and Common Pitfalls to Avoid

Knowing the legal paperwork is one thing, but actually negotiating a fair deal—and dodging the traps that can sink your financial future—is a whole different ballgame. When you’re dividing retirement funds in a Kingwood divorce, the strategy you use can mean the difference between a secure retirement and years of regret.

One of the most powerful tools we often use for our clients is the “asset offset.” It’s a straightforward concept: you trade your interest in a retirement account for another asset of equal value.

For instance, many of our Kingwood clients want to keep the family home, especially if they have kids. Let's say the community property portion of your spouse's 401(k) is worth $150,000, and you have $150,000 in home equity. You might agree to let your spouse keep their entire 401(k) if you get the house free and clear of their claim. It can be a win-win, but only if the valuations of both assets are spot-on.

Common Pitfalls That Can Derail Your Settlement

While a good strategy sets you up for success, a simple mistake can unravel everything. Being aware of these common missteps is your best defense. We see it all the time with people divorcing in the Kingwood and Northeast Houston area—small oversights that turn into huge problems down the road.

Here are some of the most frequent (and costly) pitfalls we help our clients steer clear of:

Forgetting Market Fluctuations: A 401(k) isn't like a bank account. Its value goes up and down with the market every single day. If your decree says you get “$100,000 as of the date of divorce” but the market tanks before the QDRO is processed, you could get much less. A properly drafted order must state how market gains and losses are handled between the divorce date and the actual payout.

Ignoring Tax Implications: Not all dollars are equal. A dollar in a traditional, pre-tax 401(k) is not the same as a dollar in a post-tax Roth IRA. You’ll owe income tax on the 401(k) money eventually. When negotiating an asset trade, you absolutely have to factor in these future tax hits to make sure it’s a fair swap.

Failing to Update Beneficiaries: This is one of the most tragic mistakes because it’s so easy to prevent. After your divorce is final, you must go in and change the beneficiary on every single one of your financial accounts. If you don't, your ex-spouse could inherit your entire retirement fund if you pass away—no matter what your will says.

A Cautionary Tale from a Porter Client

A few years back, a woman from Porter came to our Kingwood office in a panic. Her divorce had been final for over a year, but she’d never seen a dime of her share from her ex-husband’s pension. It turned out her previous attorney never actually drafted or filed the QDRO.

Crucial Takeaway: The divorce decree itself does not divide retirement money. The plan administrator has no legal authority to release funds without a separate, court-approved QDRO. Your share of the money is stuck in limbo until that happens.

By the time she found us, her ex was about to retire and had moved out of state. It was a logistical nightmare. For a frightening period of time, it looked like she might lose her entire six-figure share. We were able to get it sorted out, but it took urgent legal action that caused her tremendous stress and extra costs—all of which could have been avoided. Her story is a powerful lesson that timely action is critical.

Negotiating retirement assets is about more than just the numbers on a statement. It requires a deep understanding of the financial and legal traps that lie in wait. To get a better handle on the bigger picture, you can learn more about how to protect assets in a divorce in our comprehensive guide.

Our local team at The Law Office of Bryan Fagan is dedicated to navigating these complex issues for you. We’re here to shield you from costly errors and fight for the settlement you deserve. Contact our Kingwood office for a free consultation to talk about the specifics of your case.

What to Do With Your Retirement Funds After the Divorce Is Final

Once the judge's signature is on your divorce decree, you've officially crossed the finish line. It's a massive moment. But when it comes to your finances, it’s really the starting line for building your new, independent life.

After all the negotiations over your retirement accounts, you now have a legal right to a portion of those funds. The next moves you make are critical for protecting that money and making it work for you. Let's walk through exactly what you need to do here in Kingwood to secure your financial future.

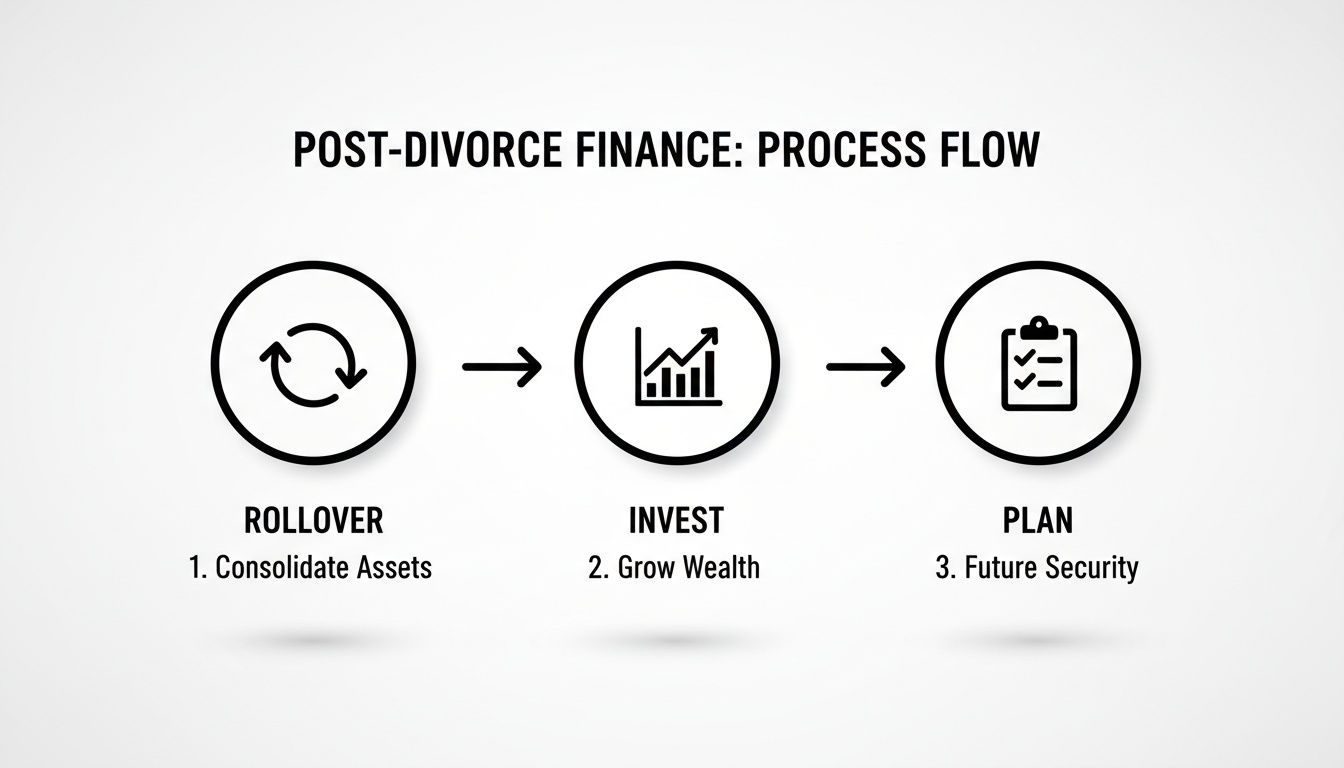

Taking Charge of Your Awarded Funds

That money can't just sit in your ex-spouse's 401(k) or pension plan. As soon as the QDRO is approved by the court and processed by the plan administrator, it’s time to move the funds into an account that is 100% in your name and under your control.

For almost everyone, the smartest move is a direct rollover into an IRA (Individual Retirement Account). This is a tax-free transfer that keeps your retirement savings growing without triggering immediate taxes or penalties. It’s a clean break, giving you full command over your investment decisions moving forward.

Think of your post-divorce financial plan as a simple, three-phase process: get control of the money, invest it wisely, and plan for your future.

Following this flow helps ensure nothing falls through the cracks as you transition to managing your own assets.

A Practical Checklist for Securing Your Money

Here are the concrete actions you need to take once the QDRO is finalized:

- Open a Rollover IRA: First, contact a financial institution to open a new IRA. Be sure to specify it's a "rollover" IRA, which is designed for this exact purpose. Local Kingwood banks or larger firms can assist you.

- Initiate the Transfer: You’ll need to provide the retirement plan administrator (your ex-spouse's employer's plan) with your new IRA account information and a copy of the approved QDRO. Your new financial institution can help you with the required paperwork for a direct rollover.

- Confirm Everything: Don't assume the transfer happened. Be proactive. Follow up with both the plan administrator and your new IRA custodian to confirm the funds have landed safely in your account.

- Meet a Financial Advisor: This isn’t a luxury; it’s a necessity. Now that the money is yours, you need a strategy. An advisor can help you invest it in a way that matches your new life goals, timeline for retirement, and comfort level with risk.

As you're organizing your new financial life, it's also the perfect time to address any lingering issues from the marriage. For example, if you filed joint tax returns, you could still be on the hook for tax debt, even if it was caused by your ex. It's worth looking into options like Innocent Spouse Relief to protect yourself.

The whole point of fighting for your share of the retirement assets in your Kingwood divorce is to set yourself up for long-term stability. It’s not just about getting the check—it’s about using it to build the secure future you deserve.

Common Questions About Dividing Retirement Funds in Kingwood

Even with a clear plan, questions will come up. When it comes to splitting retirement accounts in a Kingwood divorce, the "what-ifs" can feel endless. Let's walk through some of the most common questions we hear from clients in Kingwood, Humble, and across our community to give you some straightforward answers.

Our goal here is to demystify the process and help you feel more confident as you face these important decisions.

What Happens to My 401(k) Loan if We Get Divorced in Kingwood?

This is a great question, and it comes up all the time. If you took out a 401(k) loan during your marriage, Texas law almost always considers it a community debt. That’s important because it directly reduces the value of the account that's up for division.

Think of it this way: say a 401(k) has a $150,000 balance, but there's a $20,000 loan still outstanding. The actual community asset isn't the full $150,000. It's the net value of $130,000. The debt shrinks the pie before it's cut.

How that loan gets repaid then becomes a major negotiating point. An experienced Kingwood divorce lawyer will help you draft a final decree that spells out exactly how that debt will be handled, so one person isn't left holding the bag.

Can I Keep My Entire Pension and Give My Spouse the House Instead?

Absolutely. This is a common strategy we often use called an "asset offset." For many of our Kingwood clients, this can be a fantastic solution, especially when keeping the family home is the number one priority.

The basic idea is that you trade your spouse's share of your pension for an asset of similar value, like the equity in the house. But—and this is a big but—the math has to be perfect.

Before you even consider this kind of trade, you need a formal, accurate valuation of both the pension's present-day value and the home's current market value. A guess or an old appraisal can lead to a lopsided deal that could cost you tens of thousands of dollars down the road.

You also have to think about the nature of the assets. Cash from home equity is available now, while a pension is a promise of future payments. It's critical to work with your attorney and a financial advisor to make sure this kind of trade truly serves your long-term financial health.

My Ex-Spouse Lives in Another State but We Are Divorcing in Texas. How Does That Work?

If your divorce is filed here in Montgomery or Harris County, then Texas community property laws govern the division of your assets. It doesn't matter where your ex-spouse lives.

The jurisdiction of the Texas court is what counts. The steps for valuing the community property portion of the retirement funds and preparing the QDRO are identical. The only real difference might be some logistical hurdles, like coordinating with an out-of-state company's plan administrator. We handle these cross-state divorces for our Kingwood clients all the time, so it's a very familiar process for our team.

How Long Does It Take to Get My Money After the QDRO Is Approved?

This is the question everyone asks, and the honest answer is: it depends. The key is having a perfectly written QDRO that sails through approval without getting kicked back by the plan administrator.

Here’s what you can generally expect for a timeline:

- Court to Plan Administrator: Once the judge signs the QDRO, our office sends it to the retirement plan for their own internal review. This step alone can take anywhere from 30 to 90 days. Big companies often have a significant backlog.

- Processing and Payout: After the plan administrator officially approves the QDRO, they start the work of actually separating the funds. This next phase can take another 30 to 60 days.

All in all, you're realistically looking at a three-to-five-month wait from the day the judge signs the order until the funds are in your new rollover account. Our team is proactive about following up with plan administrators to push the process along and tackle any small issues before they become major delays for you.

Working through the complexities of dividing retirement accounts in a Kingwood divorce is much easier with someone in your corner who knows the local courts and the financial nuances. At The Law Office of Bryan Fagan – Kingwood TX Lawyers, we are a local, client-focused firm that provides trusted representation right here in our community. We focus on providing clear, practical guidance to protect your financial future.

If you have more questions or you’re ready to talk about your specific situation, we invite you to schedule a free, no-obligation consultation at our Kingwood office. You can learn more about how our Kingwood attorneys can help you by visiting us online or giving us a call to get started. We are here to help our neighbors in Kingwood, Humble, Porter, and Northeast Houston.