Skip to content

Skip to content

A lot of people in Kingwood reach the same point before they ever call a lawyer. They're sitting at the kitchen table, looking at a mortgage statement, a couple of credit card bills, a car payment, and maybe a medical balance, wondering one hard question: what happens to debt in divorce texas kingwood?

The stress isn't only legal. It's personal. One spouse may be staying in the house near Kingwood Drive. The other may be moving into an apartment in Humble or closer to work in Northeast Houston. Both are trying to figure out who pays what, what the court can order, and whether a late payment by one person can hurt the other later.

Texas law gives a framework for this, but the framework doesn't always match what people expect. Many assume debt follows the name on the bill, or that the divorce decree ends all joint responsibility. In real life, it's more complicated than that. Debt division in a Texas divorce involves property rules, fairness standards, creditor rights, and practical decisions about refinancing, account closures, and future credit protection.

That's why it helps to walk through this step by step, in plain language.

Navigating Debt When Your Marriage Ends in Kingwood

Take a common Kingwood situation. A couple owns a home, one drives the family SUV, both used a joint credit card for groceries and school expenses, and one spouse has an older student loan from before the marriage. Separation starts, and suddenly every bill feels like a problem.

The mortgage still comes due. The car lender still expects payment. The credit card company doesn't care that the relationship has changed. Meanwhile, each spouse may be asking the same thing from different angles. One asks, “Will I be stuck with debt I didn't create?” The other asks, “If the court says my spouse has to pay it, am I safe?”

Texas gives judges a way to sort debt as part of the overall divorce. The starting point is that debt tied to the marriage is often treated as part of the marital estate, and the court divides that estate under Texas rules. For families in Kingwood, Porter, and Humble, that means debt usually isn't handled as a side issue. It's part of the full property division.

Debt in divorce isn't just about who used the card or who opened the account. It's often about when the debt arose, what it paid for, and how the court balances the whole picture.

That can feel overwhelming, but it also means there's a structure. Once you understand how Texas classifies debt and how courts approach fairness, the pile of bills starts to look less like chaos and more like a set of legal and financial issues that can be addressed one by one.

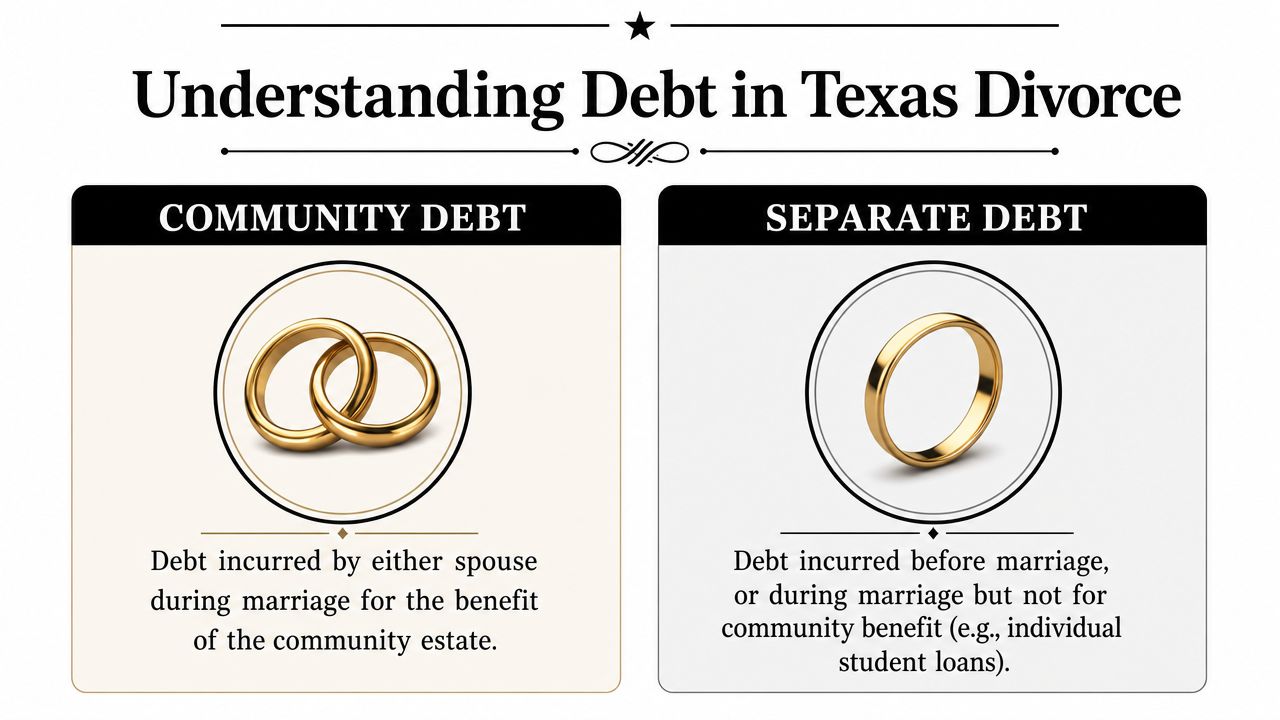

Understanding Community Debt vs Separate Debt in Texas

A helpful starting point is to sort debt the same way you would sort boxes during a move. Some boxes clearly belong to the household. Others clearly belong to one person. Texas divorce debt works in a similar way, although the legal labels can make it feel more complicated than it really is.

In broad terms, debt tied to the marriage is often treated as community debt. Debt that belongs to one spouse alone may be treated as separate debt. The tricky part is that the answer does not always depend on whose name is on the statement. It often depends on timing, purpose, and whether the debt served the marriage.

What community debt usually means

Community debt usually refers to obligations connected to married life. If debt was taken on during the marriage to pay for ordinary family needs, there is a good chance it will be treated as part of the marital financial picture.

For many Kingwood families, that includes debts such as:

- Mortgage used for the family home: Usually handled as part of the overall marital estate.

- Joint credit cards used for groceries, utilities, school costs, or home repairs: Often viewed as debt that benefited the household.

- Car loan for a vehicle used by the family during the marriage: Commonly considered alongside other shared finances.

That does not mean each spouse will automatically pay half. It means the debt goes into the larger pile the court or the spouses must sort out.

What separate debt usually means

Separate debt usually has a clearer connection to one spouse alone. A debt from before the wedding is the easiest example. Another common example is a debt incurred during the marriage for a purpose that did not really benefit the household.

Examples include:

- A student loan taken out before marriage

- A credit card balance carried into the marriage

- A personal obligation tied mainly to one spouse's individual purpose

Confusion often arises regarding this point. An account can be in one spouse's name and still be argued as connected to the marriage if the money was used for family living expenses. The reverse can also happen. A debt created during marriage may still be argued as more personal in nature if it served only one spouse and not the household.

A quick comparison for your own notes

| Type of Debt | Typically Classified As | Example for a Kingwood Family |

|---|---|---|

| Mortgage on marital residence | Community debt | Home loan on the house where the family lived in Kingwood |

| Joint household credit card | Community debt | Card used for groceries, utilities, and kids' expenses |

| Auto loan during marriage | Community debt | Loan on the SUV used for commuting around Northeast Houston |

| Student loan from before marriage | Separate debt | Degree loan one spouse already had before the wedding |

| Pre-marriage credit card balance | Separate debt | Balance carried into the marriage from earlier spending |

| Personal debt with little marital benefit | Often argued as separate debt | Obligation one spouse took on for an individual purpose |

Why this distinction matters in real life

Classification matters because it shapes your strategy from the beginning. It affects what records you gather, what arguments make sense, and what kind of settlement may protect you best after the divorce is final.

It also matters for a reason many people do not see at first. A divorce decree can assign a debt to your former spouse, but that does not automatically erase your name from a joint account or stop a lender from trying to collect from you. In other words, the court can divide responsibility between spouses, but the creditor still looks to the original contract.

That disconnect is where real financial trouble often starts.

If you are sorting debts alongside the rest of your marital assets, it helps to review how courts handle the bigger picture in property division in a Kingwood divorce.

Practical rule: Make a list of every debt and write down three facts beside each one: when it started, whose name is on it, and what the money was used for. That simple chart often shows which debts are likely to be disputed, and which ones may still affect your credit even if the decree assigns payment to the other spouse.

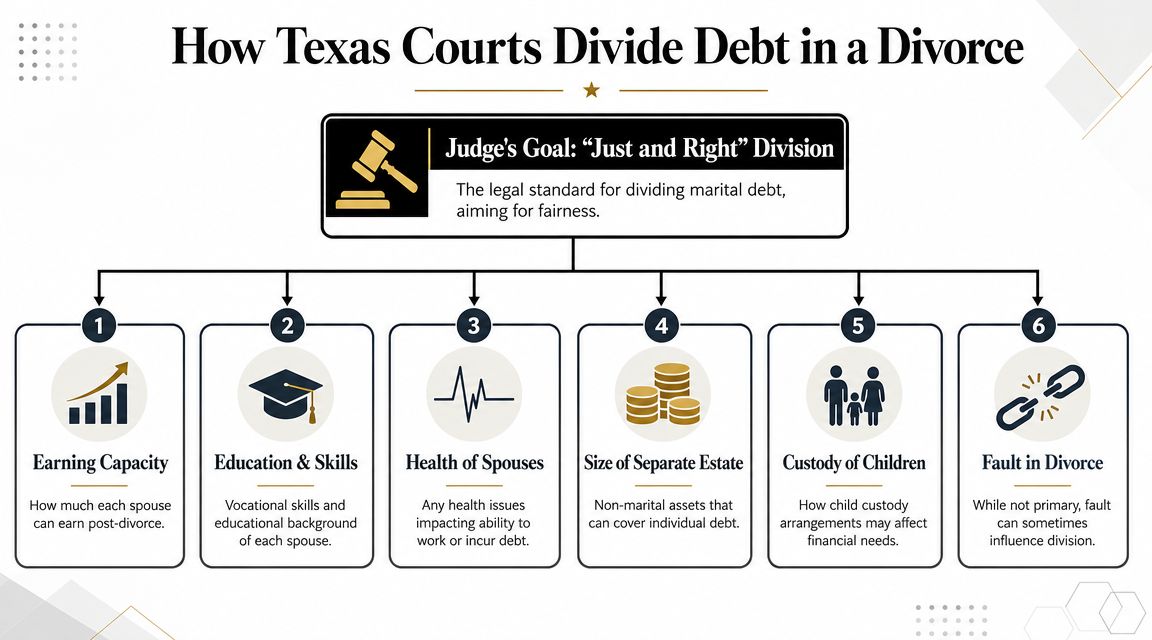

How Texas Courts Divide Debt in a Divorce

A lot of Kingwood spouses come into divorce with a simple assumption. If there are two people, the court will split the debt in half.

Texas courts do not use that kind of fixed formula. In a divorce, the judge looks for a division that is just and right under the facts of that family. Sometimes that ends up close to even. Sometimes it does not. Fairness in a Texas divorce is more like balancing a scale than cutting a pie into identical slices.

Judges look at debt as part of the full property division

A court usually does not examine one credit card or one loan by itself. It looks at the full financial picture. That includes the house, vehicles, bank accounts, income, monthly expenses, and who is leaving the marriage in a stronger or weaker position.

In practical terms, a judge may consider:

- Who took on the debt and why

- Whether the debt benefited the marriage or mainly one spouse

- Which spouse is keeping the asset tied to the debt

- Each spouse's ability to make the payments after divorce

- Whether one spouse will have more child-related or household expenses

- How the rest of the assets and debts are being divided overall

That is why debt division rarely works like a calculator. It works more like a household budget review.

A court may divide debt unevenly and still be acting fairly

Suppose a couple has a home loan, an auto note, and several credit card balances. One spouse earns more. The other will be covering more day-to-day expenses for the children after separation.

A judge may decide the higher-earning spouse should take more of the marital debt. In another case, the spouse keeping a valuable asset may also take the loan attached to it. The result can look uneven on paper while still making sense in real life.

That point matters because many people focus only on the total amount assigned to each side. The court is usually asking a different question. Who can carry this debt after the divorce without setting up a future default?

Debt attached to property often stays with the property

Secured debt gets special attention because it is tied to something specific, like a house or a car. If one spouse keeps the home, the mortgage often follows the home. If one spouse keeps the vehicle, the car loan often follows the vehicle.

That sounds straightforward, but only inside the divorce case.

Outside the divorce case, the lender still cares about the names on the original contract. So if your spouse is awarded the car and ordered to pay the note, but your name stays on the loan, the court has settled responsibility between the two of you. It has not changed the lender's rights. For many Kingwood families, that is the gap that causes trouble later.

What judges often want to see

Courts tend to respond better to debt proposals that are practical and specific. A plan carries more weight when it answers real-world questions instead of just saying, “each party pays half.”

For example:

Who is keeping the asset connected to the debt?

If the proposal separates the asset from the loan, there should be a clear reason.Can the spouse taking the debt afford it?

A payment assignment only works if the numbers work.Is refinancing possible within a realistic time?

If the plan depends on refinancing, it helps to know whether that is likely or just hopeful.Does another part of the property division offset the debt load?

One spouse may take more debt because they are also receiving more property or more income-producing assets.What happens if the debt is not paid?

A strong decree often includes deadlines, indemnity language, and steps to reduce future disputes between former spouses.

A simple way to judge whether a proposed split makes sense

Ask yourself two questions.

First, does this division seem fair inside the divorce? Second, does it reduce risk outside the divorce?

Those are not the same thing. A proposal may look fair because it assigns a joint credit card to the spouse who used it more. But if the account stays open and your name stays on it, you may still carry financial exposure after the decree is signed. That is why debt division should be judged by both the courtroom result and the practical outcome.

The best debt plans do both. They divide responsibility fairly, and they also reduce the chance that an old joint account will follow you into post-divorce life.

The Real-World Impact on Your Credit and Joint Accounts

This is the part many people don't hear until they're already dealing with damage.

A divorce decree can assign debt between spouses, but a Texas Final Decree of Divorce does not bind third-party creditors. If both spouses are on a loan, the lender can pursue either one regardless of what the decree says, and Texas Law Help's guidance on dividing property and debt in divorce explains that this is why a decree may require refinancing to remove a spouse's name.

That rule creates the biggest disconnect in debt division.

The decree and the creditor are not the same thing

The family court controls the legal relationship between spouses. It can say, “Spouse A must pay the car loan.” But the lender controls the contract. If both spouses signed that contract, the lender may still seek payment from either one if the account falls behind.

This catches people off guard in Kingwood, Porter, and Humble all the time. They assume the decree solved the problem. It may have solved the issue between the spouses. It may not have solved the issue with the bank.

A simple car loan example

A couple divorces. The husband keeps the car and the decree says he must pay the auto note. The wife's name stays on the loan because refinancing doesn't happen.

Months later, he misses payments.

The lender may still report the late payments on an account connected to her name and may still pursue collection from her, even though the divorce order assigned him the debt. She may have a claim against him for violating the decree, but that doesn't erase the creditor's rights in the meantime.

That's why debt division is not only a legal allocation problem. It is also a credit exposure problem.

Joint accounts can stay dangerous after the divorce

The same issue comes up with mortgages, joint credit cards, and other accounts held in both names. Risks include:

- Late payment damage: One missed payment can affect the other spouse's credit if the account remains joint.

- Continued account use: If a joint credit card stays open, new charges can create fresh disputes.

- Collection activity: A collector may contact the spouse the decree did not assign as responsible if that spouse remains on the contract.

For a family trying to rebuild after divorce in Northeast Houston, this can delay housing plans, car purchases, or even routine financial recovery.

The divorce decree can say who should pay. The lender still looks to who promised to pay.

Why refinancing matters so much

Refinancing is often the cleanest way to separate future risk. It may remove one spouse from a mortgage, auto note, or another financed account. But refinancing isn't always available. Income, debt-to-income ratios, property value, and credit history all affect whether a lender will approve it.

That means a good divorce plan doesn't stop at “you take this debt.” It asks harder follow-up questions:

- Can the loan be refinanced?

- By when?

- What happens if refinance is denied?

- Is sale of the property the backup plan?

- Should a joint credit card be closed instead of left open?

Those practical questions often matter more than the broad legal principle. They're what protect your day-to-day finances after the paperwork is signed.

Practical Steps to Protect Your Finances During a Divorce

Once divorce becomes likely, waiting usually makes debt problems harder to control. The goal is to create a financial firewall around yourself without violating court orders or creating unnecessary conflict.

The Consumer Financial Protection Bureau noted in 2024 that medical bills were a major source of debt collection actions and finalized rules in 2025 limiting their inclusion on credit reports, as discussed in the CFPB announcement on medical bills and credit reports. For someone divorcing in Kingwood or Humble, that shifting collection environment is a reminder to act early, especially if medical debt or unsecured consumer debt is in the mix.

Start with a paper trail

Before you negotiate anything, gather records. Not later. Now.

Use a folder, a secure cloud drive, or both. Collect:

- Recent account statements: Mortgage, credit cards, auto loans, personal loans, and medical balances.

- Tax records and pay information: These help show the bigger financial picture.

- Loan documents: Look for who signed, what secures the debt, and whether there are payoff or refinance details.

- Credit reports: These can reveal accounts one spouse forgot to mention or debts that have already gone to collection.

If you need a broader guide to reducing financial risk around marital property, this discussion of divorce asset protection strategies offers useful ideas that also highlight why early organization matters.

Make immediate account decisions carefully

Not every joint account should stay open while the divorce is pending. But don't act recklessly. Temporary orders, automatic standing orders, or practical household needs may affect what should be closed first.

A careful checklist often looks like this:

Review every joint credit card

If a card can be frozen, restricted, or closed without disrupting essential expenses, that may reduce the chance of new marital debt.Open an individual banking account

Deposit your income into an account you control once your lawyer confirms the timing and approach make sense.Change online passwords

Update banking, credit card, email, and cloud storage credentials for your own accounts.Set payment alerts

Lenders and card issuers often let you receive email or text alerts for missed payments or balance changes.

Important note: Protecting yourself doesn't mean hiding money or draining accounts. Courts care about that distinction, and so do judges in this area.

Build a realistic post-separation budget

People often focus on who gets which debt without first asking whether the payment plan is sustainable. A budget won't solve everything, but it helps you recognize what you can carry.

Include housing, utilities, food, transportation, insurance, school costs, medical needs, and minimum debt payments. If a proposed settlement assumes you can carry the house, the car, and several credit cards, your budget may show that the proposal is unrealistic.

Monitor your credit while the case is open

Divorce is not a single event. It's a period of change. During that time, joint accounts may be used, balances may move, and collectors may become more active.

Monitor for:

- Late payments on shared accounts

- Unexpected balance increases

- New collection activity

- Accounts you didn't know existed

For local help with these issues, some people work with a financial professional, while others also consult a lawyer focused on debt and property planning. For those in Kingwood, how to protect assets in a divorce is a useful local resource. The Law Office of Bryan Fagan – Kingwood TX Lawyers also handles divorce and property division matters that include debt-related planning.

Negotiating Debt in a Divorce Settlement Agreement

Court is not the only path. Many couples in Kingwood, Humble, and Northeast Houston resolve debt issues through negotiation, mediation, or informal settlement discussions before a judge ever makes the final call.

That can be a good thing. A negotiated agreement often gives both spouses more control over timing, trade-offs, and practical solutions.

Good negotiation starts with likely court outcomes

A settlement works best when both sides understand what a judge might do if no agreement is reached. Texas courts often use an equitable approach where debt allocation tracks the associated asset, and the spouse who keeps the house is typically assigned the mortgage, according to this discussion of debt division in divorce.

That principle gives structure to settlement talks.

If one spouse wants the house in Kingwood, that spouse usually needs to be prepared to discuss the mortgage, refinance options, taxes, insurance, and what happens if refinance fails. If one spouse wants the vehicle, the same logic usually applies to the car note.

Smart settlements use trade-offs

Debt negotiation is rarely about debt alone. It's about the full package.

A workable settlement might involve:

- One spouse taking more unsecured debt in exchange for more liquid assets

- One spouse keeping a financed asset and taking its related loan

- Both spouses agreeing to sell property rather than forcing a risky refinance

- A deadline for payoff or refinance with a backup remedy if that deadline isn't met

That's where careful drafting matters. A vague agreement creates future conflict. A detailed one addresses timing, account closure, refinance obligations, and what each spouse must do if a lender refuses to cooperate.

Bankruptcy and divorce can intersect

Some families are not only dividing debt. They're trying to decide whether the debt load is manageable at all. In those situations, it can help to understand the wider timing questions around financial decisions during divorce or bankruptcy, because the order in which those issues are addressed can affect strategy.

That doesn't mean every divorce with debt should involve bankruptcy. It means debt settlement choices should be made with full awareness of the broader financial situation.

A strong settlement is not the one that sounds fair in the conference room. It's the one that still works when the first mortgage statement arrives after the divorce.

What to push for in a written agreement

When negotiating debt terms, clarity protects both sides. Look for language that addresses:

| Issue | Why it matters in settlement |

|---|---|

| Specific debt assignment | Avoids later arguments about who was supposed to pay |

| Refinance deadline | Sets a firm point for removing a spouse from liability if possible |

| Property sale backup plan | Gives a path forward if refinance doesn't happen |

| Indemnity language | Helps address what happens if one spouse causes financial harm by nonpayment |

| Account closure terms | Reduces the risk of fresh charges after separation |

A settlement can be more flexible than a court ruling, but only if it's drafted with real-world problems in mind. In many cases, negotiation is where spouses can build a better answer than either a rough compromise or a generic decree.

Why You Need a Kingwood Family Law Attorney for Debt Division

Debt division looks simple from a distance. List the accounts. Split responsibility. Move on.

But people in Kingwood usually learn quickly that the hard part isn't making a list. The hard part is protecting themselves from what happens after the list is written.

Where legal help becomes hard to replace

Some situations call for more than general advice from friends or internet research.

For example:

- A house can't be refinanced easily: One spouse wants to keep it, but lender approval is uncertain.

- A spouse may be hiding debt: Accounts appear on a credit report that weren't disclosed.

- Business or investment debt is involved: Those obligations may be tied to property that needs careful valuation and division.

- A creditor keeps pursuing both spouses: Even after temporary agreements or a signed decree.

- A settlement sounds fair but is poorly drafted: The language doesn't explain deadlines, backup plans, or enforcement options.

A family law attorney helps identify those risks before they become expensive surprises.

A lawyer does more than file papers

In debt-related divorce cases, an attorney often acts in three roles at once.

First, they help classify what you're dealing with. Which obligations are likely marital, which may be separate, and which need closer proof.

Second, they help build strategy. If your spouse keeps the house in Kingwood, should there be a refinance deadline? If a joint card remains open, should closure be mandatory? If your credit is exposed, what language belongs in the decree?

Third, they help negotiate and enforce. If your spouse doesn't follow the order, or if settlement terms are too vague to protect you, legal guidance becomes more than helpful. It becomes protective.

A good starting point for anyone comparing legal options is this local guide on how to choose a divorce attorney.

For readers who want a short overview of how these issues play out in practice, this video is worth watching.

Local context matters

A lawyer who regularly works with families in Kingwood, Humble, Porter, and Northeast Houston understands the practical side of these cases. Mortgage issues, commuting vehicles, school-related expenses, and local property concerns often shape what a workable debt plan looks like.

That local perspective matters because debt division is not just legal theory. It affects where you live, what you can refinance, and how quickly you can rebuild.

If you're asking what happens to debt in divorce texas kingwood, the honest answer is that it depends on the type of debt, the broader property division, your contract exposure, and how carefully the final agreement is built. That's exactly why legal help is an investment in your financial future, not just another line item during an already stressful time.

If you're facing divorce in Kingwood and you're worried about the mortgage, credit cards, car loans, or joint accounts, talk through your situation with Law Office of Bryan Fagan – Kingwood TX Lawyers. A free consultation can help you understand your options, spot financial risks early, and build a plan that protects your future in Kingwood, Humble, Porter, or Northeast Houston.