If you've changed jobs, gone through a divorce, remarried, or opened a retirement account years ago and never looked at the paperwork again, there's a real chance your assets won't go where you think they will. I see this issue all the time with families in Kingwood, Humble, Porter, and Northeast Houston. They have a solid will, or at least they think they do, but an old beneficiary form is sitting on a 401(k), IRA, or life insurance policy and pointing the money somewhere else.

That mismatch creates some of the ugliest estate disputes in Texas because it feels unfair and completely avoidable. It usually is.

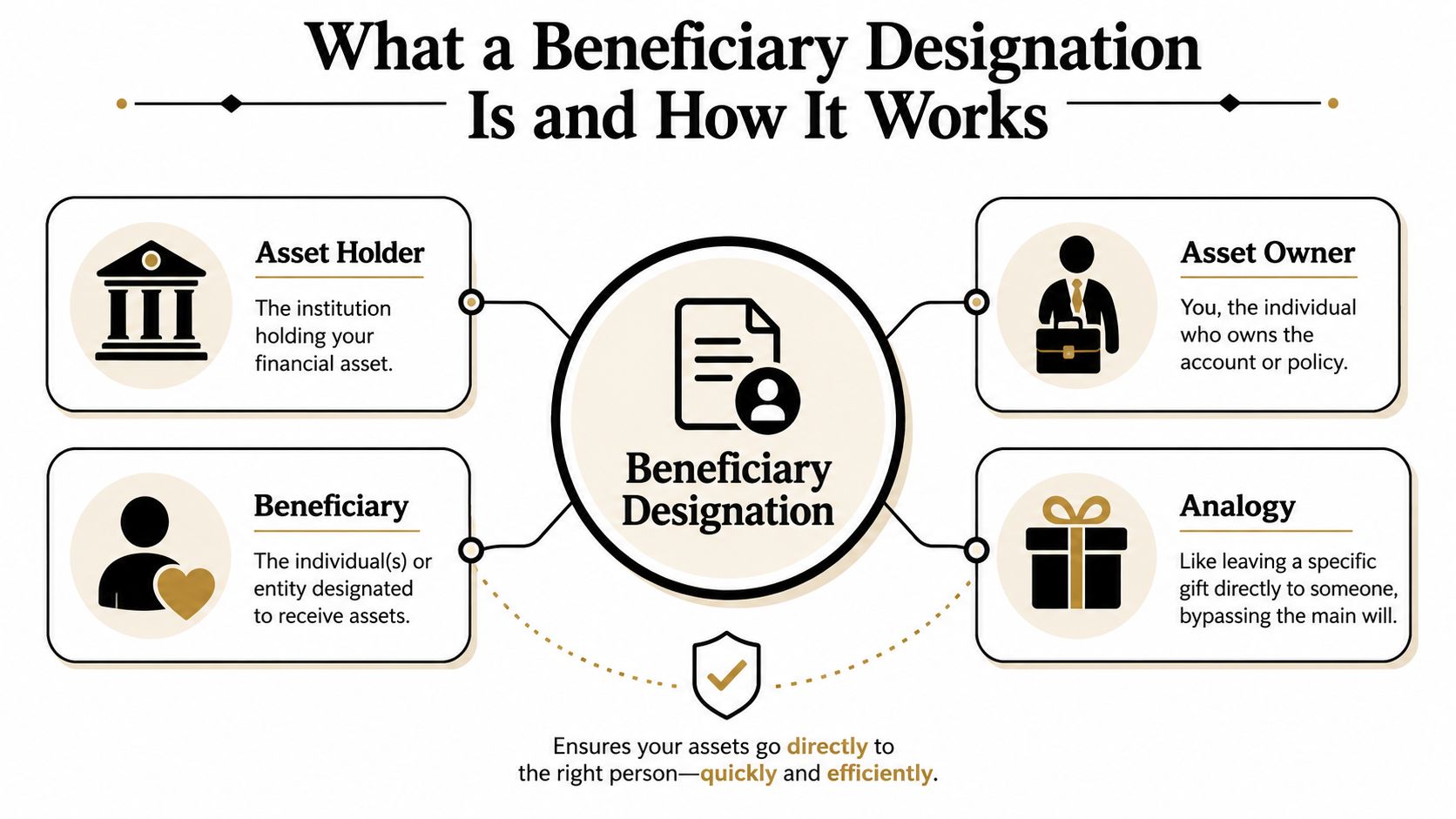

If you're asking what is beneficiary designation, the short answer is simple. It's the instruction attached directly to certain financial accounts that tells the company who gets that asset when you die. In many cases, that form has more practical power than the will people spent time and money preparing. If you live in Kingwood and want your estate plan to work the way you intend, you need to understand this.

What a Beneficiary Designation Is and How It Works

A beneficiary designation is a direct instruction tied to a specific account or policy. According to Bentley's explanation of beneficiary designations, it is a contract-based instruction on an eligible financial asset that directs the institution to transfer the asset at death to the named person or organization, and it generally operates outside probate and outside the will or living trust.

The easiest way to think about it is this. Your will is a broad set of instructions. A beneficiary designation is a note clipped directly to one account that says, “When I die, this goes to this person.”

That note usually controls.

Which assets usually have beneficiary forms

In Kingwood estate planning meetings, people are often surprised by how many accounts fall into this category. Common examples include:

- Retirement plans: 401(k)s, IRAs, and similar retirement accounts often require a named beneficiary.

- Life insurance policies: The insurance company pays the person or people named on the policy records.

- Annuities: These contracts commonly include beneficiary instructions.

- Bank accounts with POD status: Payable-on-death accounts transfer to the named recipient.

- Investment accounts with TOD status: Transfer-on-death registrations work in a similar way.

If you're sorting out whether an asset bypasses probate, this guide on non-probate assets in Texas is a useful starting point.

What the form usually asks for

These forms are more formal than people expect. In practice, they often require a beneficiary's full legal name, date of birth, and a stated share. Many providers also require the total allocation to equal 100%, and some systems require percentage allocations in whole numbers, as described in this public benefits beneficiary help page.

Practical rule: If your form is incomplete, vague, or inconsistent, you are creating delay for your family.

You can usually name both primary beneficiaries and contingent beneficiaries. Primary beneficiaries inherit first. Contingent beneficiaries are backups if the primary beneficiary can't inherit.

For a plain-language outside perspective, Federal Benefits Sherpa has critical information on designating beneficiaries that many readers find helpful before they sit down to review their own accounts.

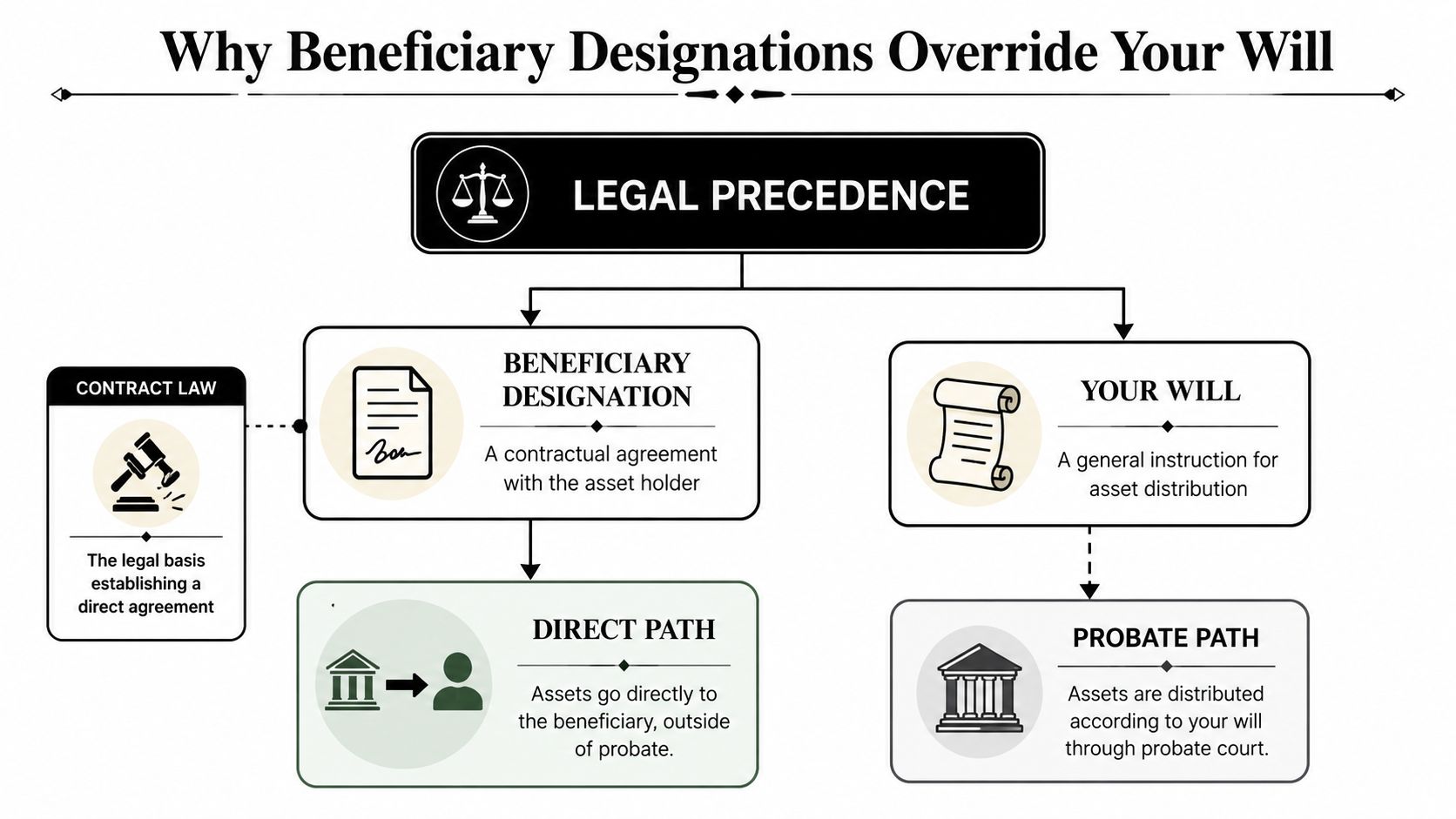

Why Beneficiary Designations Override Your Will

This is the part people in Humble and Northeast Houston most often get wrong. They assume the will is the final word on everything. It isn't.

A beneficiary designation usually wins because the asset passes under the contract you signed with the financial institution, not under the instructions in your will. Schwab explains that a beneficiary designation is a contract-based instruction, it typically overrides a will for those specific assets, and it usually avoids probate, allowing faster distribution to named recipients in Schwab's beneficiary overview.

The company holding the account doesn't start by reading your will. It starts by checking its own records.

That's why these assets are often called non-probate assets. If you want a local explanation of the difference, review probate and non-probate assets in Texas.

A common example that causes real trouble

Suppose a father in Kingwood signs a will leaving everything equally to his children. Years earlier, during a prior marriage, he named his then-spouse as beneficiary on his retirement account. He gets divorced, updates the will, but never updates the retirement account form.

When he dies, the old beneficiary form may still control that account.

That result shocks families because they think the newer will should fix the problem. It often doesn't. The account custodian follows the most recent valid beneficiary designation on file.

Why people use beneficiary designations anyway

They aren't bad. In fact, they're useful. They often let assets transfer more directly and with less delay than a court-supervised probate process.

That's one reason estate plans should coordinate wills, trusts, and beneficiary forms instead of treating them like separate projects. If you're comparing those tools, Cremation.Green has a helpful guide to family asset protection through wills and trusts.

For divorcing spouses, this issue overlaps with property division. A Property Division Lawyer in Kingwood handles division of community property and complex assets for Kingwood divorces, which often includes reviewing who owns the asset and who is still listed to receive it.

Texas Law and Your Beneficiary Choices

Texas adds another layer. This state follows community property rules, and that changes how you should think about beneficiary designations during marriage, divorce, and remarriage.

A generic online article might tell you to “just name a beneficiary.” That's not enough for many families in Kingwood, Porter, and Northeast Houston. Western & Southern notes that an overlooked issue is how beneficiary designations interact with divorce, remarriage, and blended families, because beneficiary forms can still control payout on retirement accounts, life insurance, and POD or TOD accounts unless they are formally changed, and those designations override the will for those accounts in its discussion of beneficiary designations.

Community property changes the conversation

If an account was built during marriage, a spouse may have rights that matter even if only one spouse's name is on the account. That's especially important with retirement funds.

Here is the practical problem. A married person in Kingwood may think, “This is my 401(k), so I can leave it to my brother.” It isn't always that simple under Texas law. If the value was accumulated during marriage, the surviving spouse may have a legal argument about community property interests.

Texas-focused advice: Don't change a beneficiary on a major account during marriage without first understanding whether the asset includes community property.

That doesn't mean you can never name someone other than your spouse. It means you shouldn't treat the form like casual paperwork.

Divorce orders and beneficiary forms must match

Divorce is where these mistakes become expensive and personal. People assume the divorce decree automatically cleans up every old beneficiary designation. Sometimes it doesn't. Sometimes one document says one thing, while the account paperwork says another.

If you're trying to keep loved ones out of court, this article on how to avoid probate in Texas helps explain where beneficiary planning fits.

An Estate Planning Attorney in Kingwood handles wills, trusts, and estate plans for Kingwood families, and that work should include reviewing how account designations line up with the rest of the plan.

Blended families need more than a quick form

Remarriage creates its own set of conflicts. A parent may want to provide for a current spouse and still protect children from a prior marriage. A simple beneficiary form may not accomplish both goals well.

In those cases, naming a trust instead of an individual can be worth discussing. So can reviewing whether different assets should go to different recipients for different reasons. The point is coordination, not guesswork.

This short video gives a helpful overview before you act on any changes.

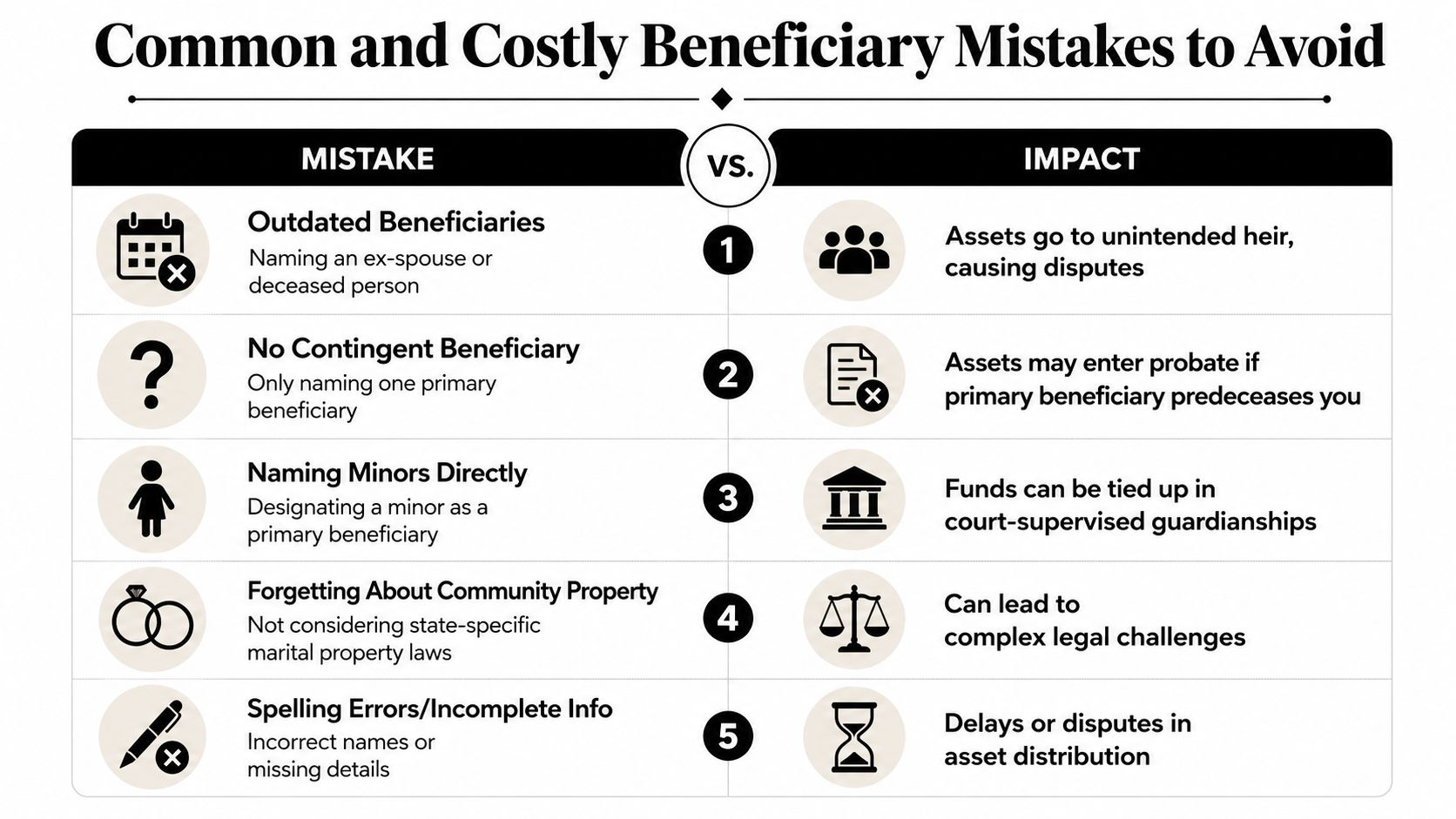

Common and Costly Beneficiary Mistakes to Avoid

Most beneficiary problems don't come from complicated law. They come from neglect. Someone fills out a form once, then life changes and the form doesn't.

Wells Fargo Advisors warns that beneficiary designations have priority over conflicting estate documents, so an outdated designation can override a later will or trust. It also notes that people should name both primary and contingent beneficiaries and update forms after major life events such as marriage, divorce, birth, or death in its beneficiary designation tips.

The forgotten ex-spouse

A man in Humble gets divorced. He updates his will and assumes he's done. He never changes the beneficiary on an old life insurance policy.

When he dies, the policy pays based on the old designation. His children are stunned, and the family ends up in a dispute that could have been prevented with one form.

The minor child mistake

A mother in Porter wants to make sure her child is protected, so she names the child directly on an account. Her intention is good, but the setup may create court involvement because a minor cannot take direct control of a substantial asset.

A better question is whether a trust or other arrangement should receive the funds for that child. If your intended beneficiary is a minor, incapacitated, or has special needs, do not guess your way through that decision.

The no-backup problem

A retiree in Northeast Houston names one primary beneficiary and stops there. Years later, that person dies first. No contingent beneficiary is listed.

Now the account may fall into probate or follow the institution's default rules. That's a terrible outcome for something so easy to prevent.

If you name a primary beneficiary, name a contingent beneficiary too.

The vague wording problem

A person writes “my children” on one account and assumes that's enough. Maybe it is. Maybe it isn't. Families change. Stepchildren may be involved. There may be adoption issues, predeceased children, or disagreements over meaning.

Use full legal names where the institution requests them. Give the information the form asks for. Precision is your friend.

The Texas marriage blind spot

This one matters more in Kingwood than many national articles admit. A spouse ignores possible community property issues and changes beneficiary forms without considering marital rights or divorce orders.

That decision can produce a legal fight between the named beneficiary and the surviving spouse. It can also derail the clean transfer the account owner thought they had created.

A quick checklist of trouble spots helps:

- After divorce: Remove and replace outdated names if the change fits your decree and your legal strategy.

- After remarriage: Review every major account, not just the new will.

- When a beneficiary dies: Update the form immediately.

- When children are young or vulnerable: Consider whether direct naming is really appropriate.

- When percentages are split: Confirm the allocations add up correctly and match your intent.

A Practical Guide to Managing Your Beneficiaries

A bad beneficiary form can lie dormant for years, then explode after a divorce, a remarriage, or a death. I have seen families assume their estate plan was fine because they signed a will, while an old retirement account or life insurance form still sent money somewhere else. In Texas, that mistake gets even more dangerous when community property rights and divorce orders are part of the picture.

Treat beneficiary review like a maintenance task. Put it on the calendar and handle it with the same care you would give a deed or a trust.

Step one: build a complete beneficiary inventory

Start with every account that can pass by beneficiary form. That usually includes retirement accounts, life insurance, annuities, bank accounts with POD designations, and brokerage accounts with TOD designations.

Create a simple chart with five items: the account, the institution, the primary beneficiary, the contingent beneficiary, and the date you last confirmed the form. Keep it plain. Accuracy matters more than format.

Step two: confirm the designation the company actually has

Memory is useless here. Your intent does not control. The form on file controls.

Log in to each account or contact the institution and ask for the current beneficiary confirmation. Read the actual names, percentages, and backup beneficiaries. If the account is tied to an old employer, an old policy, or an account you rarely check, pay extra attention. Those are the ones that cause trouble.

Step three: review Texas-specific risk points

Generic advice proves insufficient here. Texas families need to ask one more question for each account: is this separate property, community property, or mixed in a way that could trigger a fight?

Use these life events as mandatory review points:

- Marriage: Review every major account, especially anything funded during the marriage.

- Divorce: Check each beneficiary form against the divorce decree. Do not assume the decree fixed every account automatically.

- Remarriage: Rework beneficiary choices so they match your current spouse, your children, and any blended family plan.

- Death of a beneficiary: Replace that person right away.

- Birth or adoption: Decide whether to name the child directly, use percentages, or direct the share through a trust if that fits your plan.

If you are married and want to name someone other than your spouse on an account that may involve community property, slow down and get legal advice before you sign anything.

Step four: match each form to the rest of your estate plan

People create contradictions. The will says one thing. The beneficiary form says another. A divorce decree says a third.

Your designations should work with your will, any trust, and any court orders already in place. If you have a blended family, a child with special needs, or property that may be partly community and partly separate, do not guess. Get the forms coordinated correctly the first time.

Step five: keep proof and store it where someone can find it

Save copies of every submitted form, every confirmation email, and every acknowledgment from the financial company. Keep those records with your estate planning documents.

Also tell the right person where the file is. A perfectly updated beneficiary designation does not help much if nobody can locate the confirmation after you die.

If you want a lawyer to review the forms and make sure they line up with your Texas estate plan, Law Office of Bryan Fagan – Kingwood TX Lawyers is one local option for beneficiary coordination and document review.

When to Contact a Kingwood Estate Planning Attorney

Some beneficiary issues are simple. Others are loaded with risk. If you're married, recently divorced, remarried, raising children from different relationships, or trying to protect a minor or vulnerable beneficiary, this isn't paperwork you should handle casually.

The hard truth is that one outdated designation can disinherit the person you meant to protect. It can also hand your family a legal fight at the worst possible time. In Texas, those fights often involve more than a bad form. They can involve community property questions, divorce language, trust planning, and competing claims between relatives.

You should contact an attorney if any of these apply:

- You have an ex-spouse listed anywhere

- You want to name someone other than your current spouse

- Your beneficiaries include minors, stepchildren, or a trust

- You aren't sure whether an account is separate or community property

- Your will and account designations were prepared at different times

Families in Kingwood, Humble, Porter, and Northeast Houston don't need more generic internet advice on this topic. They need a coordinated Texas plan that works in real life.

A short review now can prevent confusion later. It can also give you peace of mind that your assets will pass the way you intended.

If you want clear answers about beneficiary designations, probate avoidance, divorce-related updates, or Texas community property issues, schedule a free consultation with Law Office of Bryan Fagan – Kingwood TX Lawyers. Our Kingwood office works with local families to review wills, trusts, and beneficiary forms so those documents work together instead of against each other.